[ad_1]

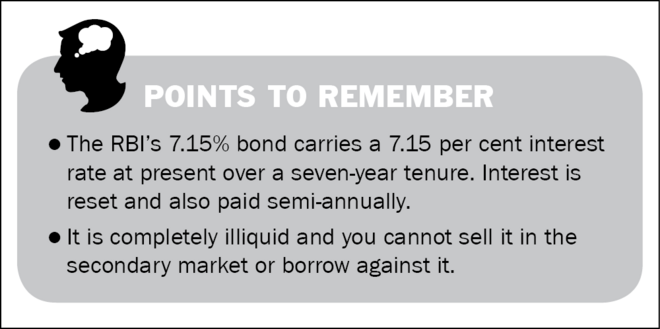

The Floating Fee Financial savings Bonds 2020 (Taxable), popularly often known as the RBI 7.15% Bonds, presently provide a 7.15 per cent taxable fee of curiosity over a tenure of seven years. They’ve changed the Authorities of India’s 7.75% (taxable) bonds – informally known as RBI 7.75% bonds. They’re known as floating-rate bonds because the rate of interest on these bonds is reset each six months ranging from January 01, 2021 and is at all times set at a diffusion of 35 foundation factors over the prevailing NSC (Nationwide Saving Certificates) fee.

Options of Floating Fee Financial savings Bonds

- Eligibility: (i) Resident Particular person, and (ii) HUF

- Entry age: There is no such thing as a minimal entry age. Within the case of minors, the floating fee bonds might be bought by dad and mom/authorized guardians.

- Investments: Minimal-Rs 1,000. Most-No restrict.

- Curiosity: 7.15 per cent (curiosity paid at half-yearly intervals on Jan 01 and July 01 yearly. There is no such thing as a choice to pay curiosity on a cumulative foundation).

- Tenure: Seven years

- Account-holding classes: (i) Particular person, (ii) Joint, and (iii) Minor by way of a guardian.

- Nomination: Facility is accessible.

- Exit choice: There is no such thing as a exit choice from these bonds earlier than maturity, apart from senior residents.

Funding goals and dangers

To supply savers with an assured fee of curiosity over the medium time period. Savers in floating fee bonds usually are not absolutely shielded from inflation.

Suitability and options

- Appropriate for conservative buyers looking for assured returns from a lump-sum funding.

- Not appropriate for buyers who can assume some threat by investing in equity-linked investments, which might generate a lot larger returns.

- Alternate options might be (i) Balanced mutual funds (for many who can assume threat), (ii) Financial institution mounted deposits, although the speed of return is decrease, and (iii) Firm deposits

Capital and inflation safety

Your capital in floating fee bonds is absolutely protected. Nonetheless, there isn’t any inflation safety, which implies each time inflation is above the newest rate of interest, the deposit earns no actual returns. Nonetheless, when the inflation is beneath the present rate of interest, it does handle a constructive actual fee of return.

Ensures

The rate of interest on floating-rate bonds is presently 7.15 per cent (topic to semi-annual reset) for a tenure of seven years.

Liquidity

These bonds usually are not listed and traded and you can’t take loans in opposition to them. You might be successfully locked in for a tenure of seven years. Nonetheless, pre-mature encashment is allowed with a penalty for senior residents after a minimal lock-in interval, which varies from 4 to 6 years relying on the age bracket by which the senior citizen falls.

For a person within the age bracket of 60-70 years, the lock-in interval is six years. If the investor is within the age bracket of 70-80, it’s 5 years and 4 years if his age is 80 or extra.

Exit choice

You may solely exit from floating-rate bonds after their maturity on the finish of seven years.

Tax implications

The curiosity on these bonds is absolutely taxable. There is no such thing as a deduction on the principal funding.

The place to purchase

They are often bought from the branches of SBI, different nationalised banks, and some other banks which have been specified by the RBI.

To view the present charges on the schemes, go to vro.in/s34211

[ad_2]

Source link

{kind=link}