[ad_1]

The viability of Japanese Mediterranean pure gasoline assets has lengthy been a supply of debate for causes together with price issues, market demand, and regional geopolitical tensions. The previous couple of years have additional difficult the controversy, introducing new questions in regards to the position of those assets in supporting post-pandemic financial restoration or serving to extra superior markets obtain net-zero insurance policies by changing coal and different gas sources (a very related subject of debate given Europe and Asia are key export targets for East Med gasoline).

The reply stays elusive. Regional gamers like Egypt, Israel, and Cyprus seem as decided as ever to get their gasoline to market, definitely motivated partially by considerations about stranded belongings in a interval when decarbonization pressures are quickly escalating. On the identical time, worldwide oil corporations stay closely engaged in regional venture improvement regardless of rising funding restrictions tied to new company local weather insurance policies. Though the financial and political prices related to a few of these initiatives are larger, these corporations are little doubt drawn to the geographic attract of the area, located on the nexus of Europe, Asia, and Africa, which presents a whole lot of export optionality.

East Med suppliers should stroll a effective line between making an attempt to capitalize close to time period on their considerable assets whereas investing in improved regional interconnectivity and expertise that can assist them create a sustainable vitality market in a decarbonizing world. The significance of the latter can’t be overstated — with no extra strategic and built-in regional technique, the present fluctuations in world gasoline markets pose an excessive amount of funding threat to massive-scale gasoline initiatives within the area with 20-30-year time horizons.

Present world competitiveness of East Med gasoline

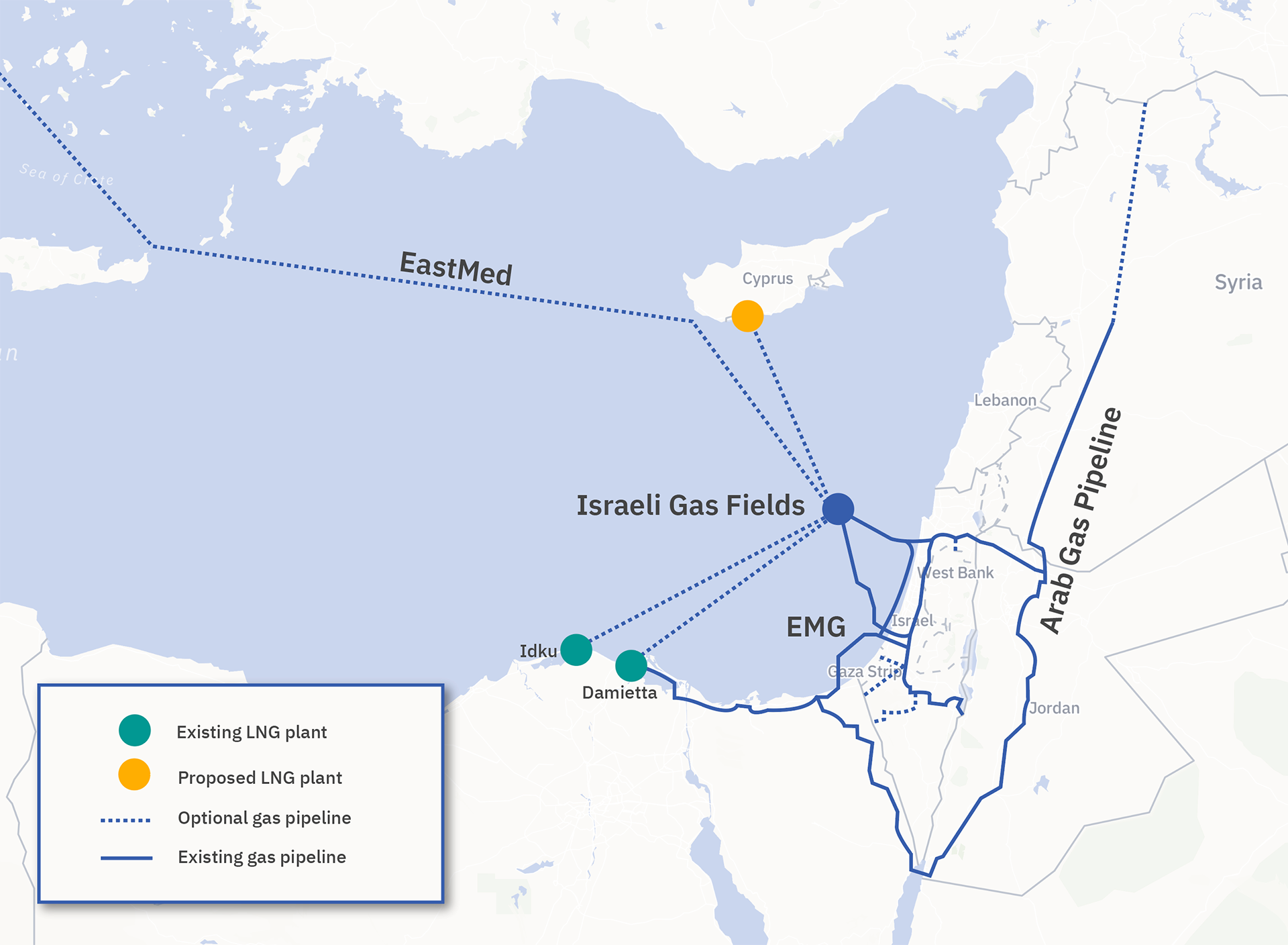

At current, Egypt is the first outlet for regional gasoline to achieve world markets within the type of liquefied pure gasoline (LNG). In response to Platts Analytics information, Egypt exported a complete of two.77 billion cu meters (bcm) and a couple of.42 bcm respectively within the first two quarters of the 12 months from its two LNG terminals, the 7.2-million-tons-per-annum (mtpa) Idku facility and the 5-mtpa Damietta plant. This clearly factors to appreciable further capability, which regional gamers are angling to fill, however importantly, Egyptian LNG can also be uncovered to identify costs, which complicates export prospects. This was notably evident over the previous 12 months when commodity costs noticed dramatic fluctuations as markets skilled uneven, post-COVID financial restoration.

Earlier this 12 months, when spot LNG costs have been within the $5-7 per metric million British thermal unit (mmbtu) vary, this was uncomfortably near breakeven costs for Egyptian LNG of round $5/mmbtu and the prevailing Egypt-Israel gasoline export settlement priced at $6/mmbtu, leaving little room for revenue. Then, as spot LNG costs hit report highs extra not too long ago — spot Asian LNG costs, for instance, have been buying and selling at round $20/mmbtu — Egyptian LNG exports might have earned sizable margins, however consumers have been altering their habits. Main spot gasoline consumers like China and India not too long ago turned to extra home gasoline, costs for that are sometimes oil-linked, to safe extra reasonably priced choices, and nonetheless different consumers have sought choices to increase deliveries inside time period contracts. In Europe, there are renewed considerations of potential gasoline shortages transferring into the winter as suppliers have been unable to fill vital storage with costs so excessive. Whereas these present pricing situations ought to have been way more helpful for East Med exports, there have been no vital new buyer-supplier channels to emerge as consumers tailored their very own habits. As world markets stutter towards restoration post-pandemic with the added dimension of rising decarbonization calls for on vitality markets, East Med suppliers must assume exterior the field relating to advertising their gasoline provides.

Past price-specific issues, regional producers must weigh their competitiveness in opposition to main nationwide oil corporations working of their key export markets like Gazprom or Qatar LNG, which profit from low-cost assets, better value flexibility, and the power to finance main initiatives like export terminals and long-distance pipelines. On this context, Asian export markets look much less real looking for the East Med given added cargo time and prices, and the abundance of LNG provides located in nearer proximity at decrease prices. East Med suppliers will possible must focus as a substitute on extra localized choices and European consumers, which would require strategic enthusiastic about modifications in European local weather insurance policies.

Europe the most effective export wager, however East Med exporters should adapt and put together to compete

The EU presents an fascinating case for East Med suppliers. Russia’s deeply entrenched pipeline connections to the market, additional bolstered by the most recent Nord Stream 2 developments, create difficult situations for newer gasoline market entrants. However, the EU stays closely engaged within the East Med and can uphold the standing of a number of main proposed regional initiatives, together with the EastMed pipeline (connecting regional assets to Greece by way of Cyprus) and the Melita TransGas Pipeline (linking Malta and Italy), as “initiatives of frequent curiosity” (PCI) that may entry EU funds by means of end-2027. The EU can also be sustaining funding for Cyprus’ deliberate gasoline import terminal at the moment beneath development.

Nonetheless, East Med producers needs to be cautious to not fall into complacency about EU assist. The EU is about to publish the EU Taxonomy Regulation earlier than the tip of the 12 months, which can comply with up on the Inexperienced Deal and not too long ago launched Match for 55 bundle to supply additional steering on the transitional position of gasoline. In 2025, it is going to evaluate the carbon border adjustment mechanism, which seeks to impose a levy on imports from carbon-intensive sectors with decrease environmental requirements than the EU. This might lead to extra direct focusing on of gasoline by means of a hefty carbon value in a matter of years.

East Med producers should look forward and take into account decreasing carbon depth to entry the EU market, whereas additionally discovering shops for their very own gasoline provides domestically to assist renewables improvement, hydrogen mixing initiatives, and different vitality transitions and regional integration initiatives that may assist long-term prospects for the trade. To some extent, the East Mediterranean Fuel Discussion board (EMGF) was established in 2019 to assist assist these aims. However the obtrusive omission of Turkey, and a number of other different regional gamers, from EMGF will possible impinge on the discussion board’s success and require continued interventions, together with from the U.S. and EU, to handle geopolitical tensions (originating not simply from Turkey, however even from Chinese language pursuits in regional energy market infrastructure) and forge forward with regional vitality initiatives.

Investments in East Med gasoline: Regional integration and considering exterior the field

Sizable gasoline investments are nonetheless deliberate for the area within the years forward, at the same time as corporations face tighter carbon restrictions and extra unsure market situations. Corporations are drawn by the massive, nonetheless untapped assets, whereas a number of the smaller or lesser-developed economies of the area are anxious for extra income streams. Alongside these initiatives, there are additionally notable investments and feasibility research being carried out to evaluate clear vitality options and tackle rising local weather considerations. The newest Intergovernmental Panel on Local weather Change report designated the East Med as notably vulnerable to local weather change with common temperatures anticipated to far exceed the worldwide 1.5 C goal. Given this confluence of pursuits, the area might want to concentrate on an all-of-the-above resolution to spice up revenues and assist financial development over the close to time period with gasoline exports whereas pursuing choices to assist clear vitality options and mitigate environmental harm for the longer term.

For now, gasoline stays on the core of any vitality technique for the area as billions of {dollars} proceed to pour into main regional initiatives. Egypt’s gas-rich deepwater and the Nile Delta stay engaging funding locations for the oil majors because the nation seeks to proceed constructing its gasoline hub standing. Phased reductions in gas subsidies have helped lend assist to gross sales costs, and assuming reforms keep the course, this could enhance attractiveness for traders.

Nonetheless, Egypt’s current 12.5-mtpa LNG export capability, and the danger that home gasoline provides may very well be inadequate to maintain up with export capability, has inspired continued dedication to different regional gasoline initiatives, together with offshore Cyprus, the place companions on the Aphrodite area (Delek, Chevron, and Shell) are nonetheless reviewing a last funding determination on a pipeline to ship gasoline from the sector to Egypt for liquefaction and export. ExxonMobil and Qatar Petroleum are to appraise their Glaucus discovery, and Whole and Eni will do the identical at Calypso (though regional disputes and the pandemic have slowed a few of these plans). Equally, in Israel, Chevron’s pursuits within the Leviathan and Tamar fields might turn into a vital feedstock supply for Egypt’s LNG crops as the corporate considers investing $235 million in a subsea pipeline venture that might double Israel’s gasoline export capability to Egypt (to assist these plans Israel is at the moment assessing whether or not to extend annual pure gasoline export quotas). Given earlier disputes with Egypt over halting gasoline exports and arrears, companions at Leviathan are additionally contemplating a floating LNG unit to keep up extra management over their very own gasoline exports.

Maybe the largest excellent funding within the area considerations the EU-backed $7 billion EastMed pipeline, meant to hold gasoline from Israel to Cyprus and Greece. The venture has its share of skeptics that query each the worth tag and the logic of a significant gasoline transport venture to Europe at a time when EU decarbonization pressures are rising so quickly. With the quantity of uncertainty about how EU local weather insurance policies and regional geopolitical tensions might impression some regional vitality ambitions, there are different, lower-cost initiatives into consideration that may very well be prioritized to advertise regional integration and use gasoline assets for advancing vitality transitions and electrical energy entry.

Regional pipelines already hyperlink key regional markets (i.e., Israel to Egypt, or Egypt or Israel to Jordan), however a brand new proposal, for instance, seems to be at choices to make use of Egyptian gasoline to produce Lebanon by way of Jordan and Syria to deal with acute energy shortages in Lebanon. Two different mega-projects search to hyperlink regional energy grids. One, the EuroAsia Interconnector, would hyperlink Israel, Greece, and Cyprus by way of a 1200-km subsea high-voltage transmission cable to finish electrical energy isolation in each Cyprus and Israel. The EU contains the venture as a PCI attributable to its potential to assist full the European Inner Market, that means the venture would qualify for financing from the Connecting Europe Facility. An analogous venture is into consideration to attach the grids of Egypt and Europe by way of Cyprus and Greece, referred to as the EuroAfrica Interconnector. These initiatives have generated notably robust curiosity due to their potential to leverage native gasoline provide to enhance regional electrification and to assist handle the intermittence of regional and European renewables initiatives.

Throughout the area, international locations are additionally introducing extra formidable renewables targets, from Greece (focusing on 65% of energy era from renewable vitality sources by 2030) to Israel (30% from renewables by 2030) and Egypt (42% of its energy from renewables by 2035, though a present proposal from the Ministry of Electrical energy and Renewable Power seeks to push that as much as 60%). Reaching these targets requires essential investments into expanded clear vitality and renewables capability, together with into hydrogen initiatives. One of the best wager for East Med producers is to pave the best way for a sustainable, regional gasoline market that helps a mixture of gasoline and renewables to maneuver towards cleaner energy era fashions and improved electrical energy entry and interconnectivity.

If the EU and world vitality majors will help facilitate the transition course of by persevering with to ramp up investments into renewables and clear tech initiatives, the area would additional acquire from transferring alongside the vitality transition curve and remaining aggressive even amid uncertainty and rising carbon restrictions in world markets.

Emily Stromquist has over a decade of expertise advising company and monetary companies shoppers on world vitality market tendencies and political threat, and has lived and labored throughout Europe, Eurasia, the Center East, and Africa. She is at the moment a Managing Director at Teneo, the worldwide CEO advisory agency, and a Non-resident Scholar with MEI’s Economics and Power Program. The opinions expressed on this piece are her personal.

Photograph by Athanasios Gioumpasis/Getty Photographs

[ad_2]

Source link

{kind=link}